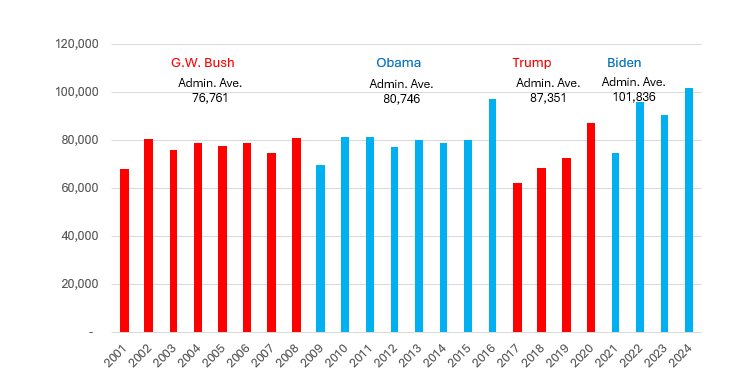

Something unprecedented happened on December 11, 2024, an event that passed with scant attention of but great importance to Americans and those regulated by the federal government. On that day, the Federal Register hit 100,000 pages in a single year. This was not even the record, but it is a noteworthy milestone. The prior record number of pages in the Federal Register in a single year was 97,110. That record was set in 2016 in the last year of the Obama Administration but was broken on December 6, 2024. Then, just a few days later, the Federal Register for 2024 broke the 100,000-page barrier.[1]

Rulemaking and Overreach

Not all rules are problematic, but the volume of federal rules is often crushing for American businesses and the customers they try to serve. In one of the more egregious examples of government overreach, the National Marine Fisheries Service (NMFS) required government minders to sail with crews on certain private fishing vessels to ensure compliance with federal laws. And here’s the kicker, the vessels themselves had to cover the costs associated with having their federal observers onboard. The government said to fisherman that you will be regulated, and you will pay for that regulation. But wait, there’s more. The NMFS then made this rule in violation of the Administrative Procedures Act. The U.S. Supreme Court was right to overturn a critical precedent earlier this year when, in Loper Bright Enterprises v. Raimondo, it overturned the most cited case in Court history, and did away with the Chevron Doctrine.

In a report issued by the Office of Management and Budget (OMB) during the Clinton Administration, the Office observed that “[r]egulations (like other instruments of government policy) have enormous potential for both good and harm. Well-chosen and carefully crafted regulations can protect consumers from dangerous products and ensure they have information to make informed choices.”[2] Ironically, the Obama Administration, which set the prior page record, used the same boilerplate language from the Clinton Administration.[3] For some administrations, this boilerplate language are mere words on a page.

Regulations (like other instruments of government policy) have enormous potential for both good and harm. Well-chosen and carefully crafted regulations can protect consumers from dangerous products and ensure they have information to make informed choice

The CFPB is an example of an agency overreach and non-action to support political expediency

Regulatory overreach outside the Bureau’s scope

The emphasis in the OMB report language should be on “well chosen” and “carefully crafted.” Sadly, many of the 100,000 pages in the Federal Register through December 11 (and the year is not done) are neither well-chosen nor carefully crafted. For example, look at the Consumer Financial Protection Bureau (CFPB). This agency has lost its bearings and has become unmoored from its statutory authority and its Constitutional requirements.

As pointed out by the U.S. Chamber of Commerce, the CFPB under Director Rohit Chopra is “harming competition and consumer choice in the financial services sector by attempting to regulate market competition, shunning procedural requirements under the Administrative Procedure Act, and devising new enforcement powers for the Director” that do not exist in law. There are other examples beyond the CFPB, but it is the agency I am most familiar with.

Regulatory under-reach inside the Bureau’s scope

In cases like those highlighted above, the CFPB takes aggressive action beyond its legal powers. In other cases, when it has the power to impact important consumer change, it chooses not to. In either case, the decisions or non-decisions rest on political expediency.

Take the CFPB complaint system. “The Dodd-Frank Wall Street Reform and Consumer Protection Act (P.L. 111-203; §1034) requires the CFPB to establish a consumer complaint system to help consumers address their complaints about consumer financial products and services in a timely manner.”[4] If properly executed, the complaint system could be a powerful tool for consumers and the businesses they use. Sadly, the best of intentions has gone very wrong.

There are longstanding and widespread concerns with the Bureau’s complaint reporting and database.[5] In letters in 2018 and 2020 to the CFPB that I wrote for the Consumer Data Industry Association (CDIA), we noted that the data in the complaint portal pertaining to the credit reporting ecosystem has a number of fundamental flaws. CDIA also offered several suggestions to make the system work as intended for consumers and businesses.[6] CDIA first identified those flaws as early as 2015, but nothing has been done before or since.

The most recent criticism of the complaint database comes from Prakash Santhana is a partner at Davies. In a 2024 piece in Corporate Compliance Insights, Santhana wrote that the CFPB complaint system

can still be manipulated, as evidenced by an investigation conducted by Davies consultants, who found that the CFPB is being infiltrated by fraudulent complaints, casting doubt on the reliability of the system at large.

Davies analysts reviewed a dataset of credit bureau complaints, paying particular attention to consumer narratives and unique zip codes. They uncovered more than 100 complaints with identical wording but different zip codes, suggesting potential system abuse by a single individual or entity.

This comment is consistent with a complaint I heard nearly a decade ago when a representative of a bank told the CFPB that consumer complaints like, “my truck could not fit through the ATM drive up window” were being counted against financial institutions. Not much has changed.

The Davies report follows a 2021 report by Oliver Wyman showing that the CFPB complaint database is being used as a tool for fraud. Despite a mountain of evidence that the CFPB can and should fix the dispute system, they refuse to do so. Sadly, the Bureau has political reasons to keep complaints artificially high.

When the Bureau can act it does not and when the Bureau cannot act, it does. This is a problem.

The power to regulate is the power to destroy

In 1819, Chief Justice John Marshall wrote that “[t]he power to tax is the power to destroy.”[7] The same is true for regulations. Businesses of all shapes and sizes can and are being crushed under the weight of regulation. As I wrote above, there are plenty of rules that are logical and necessary, but many are foolish and lack a basis in law.

As we “celebrate” the record-breaking number of pages in the Federal Register and note that the pages have climbed above 100,000 for the first time, agencies should put action to what at times has been mere words: r]egulations (like other instruments of government policy) have enormous potential for both good and harm. Well-chosen and carefully crafted regulations can protect consumers from dangerous products and ensure they have information to make informed choices.

[1] Interestingly, since 2009, the number of pages in the Federal Register tends to rise dramatically in presidential election years. This was true for Obama in 2012 and 2016, Biden in 2024, and even Trump in 2020.

[2] Office of Mgmt. & Budget, Report to Congress on the Costs and Benefits of Federal Regulations, https://clintonwhitehouse3.archives.gov/omb/inforeg/chap1.html.

[3] Office of Mgmt. & Budget, Report to Congress on the Costs and Benefits of Federal Regulations https://obamawhitehouse.archives.gov/omb/inforeg_chap1.

[4] Cong. Research Service, CFPB Consumer Complaints: U.S. and Congressional District Data, Feb. 2, 2024, https://crsreports.congress.gov/product/pdf/IN/IN12315.

[5] See, e.g., Hester Pierce and Vera Solimon, Disclosure of Consumer Complaint Narrative Data¸ Mercatus Center (Sept. 10, 2014), www.mercatus.org/publication/disclosure-consumer-complaint-narrative-data, Rachel Witkowski, Errors Abound in CFPB’s Complaint Portal, American Banker (November 17, 2015), https://www.americanbanker.com/news/errors-abound-in-cfpbs-complaint-portal.

[6] https://www.regulations.gov/comment/CFPB-2018-0006-0235, and https://www.regulations.gov/comment/CFPB-2020-0013-0093.

[7] McCulloch v. Maryland, 17 U.S. 316, 426 (1819),